According to a recent study published by CoinDesk, blockchain technology is poised for rapid expansion, generating significant interest in its diverse applications. This Beginner’s Guide to Understanding Blockchain Technology aims to demystify blockchain, covering its history, key components, benefits, limitations, and practical uses across various industries. Whether you’re a tech enthusiast, a business owner, or simply curious about the future of technology, this guide will equip you with the knowledge you need to navigate the world of blockchain.

What is Blockchain Technology?

Blockchain is a decentralized, distributed digital ledger that securely records transactions and data across a network of computers. Each confirmed transaction is grouped into a block, which is then cryptographically linked to other blocks to form a chain. Think of blockchain as a digital book shared across multiple computers, updated in real-time, and validated by a network of nodes. This ensures secure, transparent, and tamper-proof data storage.

Database vs. Blockchain

While both databases and blockchains store data, they operate differently:

- Databases: Traditional databases organize data in tables that users can easily modify. They are typically owned and managed by a single entity, leading to centralized control.

- Blockchains: In contrast, blockchains group data into blocks that form a chain. No single entity controls a blockchain; instead, it is accessible to authorized users, making it a decentralized system. This unique structure is why blockchain technology is often referred to as Distributed Ledger Technology (DLT).

Key Components of Blockchain Technology

To better understand blockchain, let’s explore its essential components:

- Blocks: Each block in a blockchain contains a set of transactions. The first block is known as the Genesis block, and subsequent blocks link to it via cryptographic hashes, forming a secure chain.

- Hashing: A hash acts like a fingerprint for each block. This unique string of characters identifies the block’s content. If any data within the block changes, so does its hash, which helps maintain the integrity of the blockchain.

- Assets: Assets can be tangible (like real estate) or intangible (like intellectual property). Blockchain can securely represent ownership and transfer of both types.

- Distributed Peer-to-Peer (P2P) Network: Transactions occur on a distributed P2P network, allowing multiple users to participate without a central authority. Each node in the network verifies transactions, enhancing security.

Types of Blockchain

Blockchain technology can be categorized based on its access and control:

- Public Blockchains: Open to anyone, public blockchains allow users to validate transactions and add new blocks. Cryptocurrencies like Bitcoin and Ethereum primarily operate on public blockchains.

- Private Blockchains: Controlled by a single organization or group, private blockchains restrict access and determine who can validate data.

- Consortium Blockchains: These are governed by a group of organizations rather than a single entity. They offer greater decentralization and are often used in industries requiring shared control.

- Sidechains: Running parallel to a primary blockchain, sidechains facilitate the transfer of digital assets between different blockchains, enhancing efficiency and scalability.

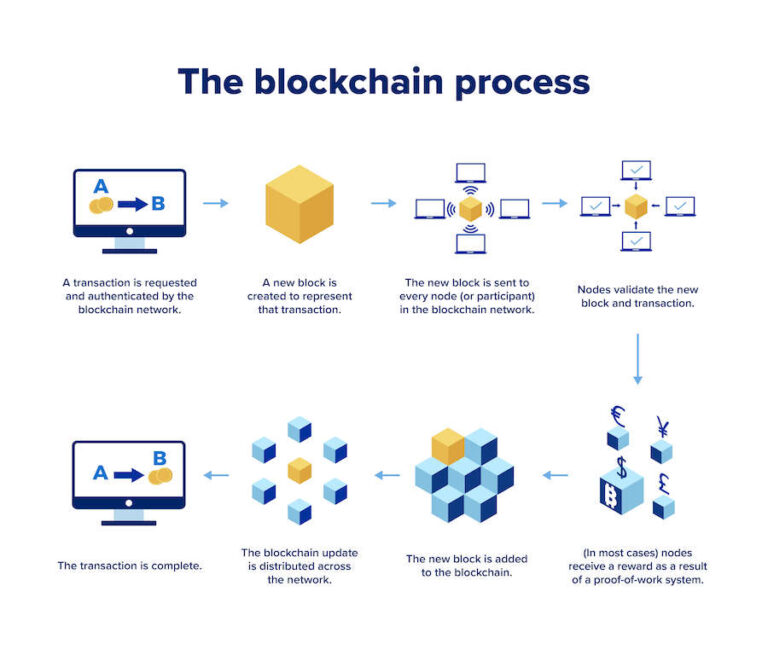

How Does a Blockchain Transaction Work?

Blockchain transactions follow a secure and transparent process:

Step-by-Step Breakdown:

- Transaction Request: A user initiates a transaction, such as transferring funds or updating records. This request is broadcasted to the network.

- Distribution: The transaction spreads across the P2P network, reaching various nodes that validate it.

- Validation: Nodes use algorithms and mathematical equations to confirm the transaction’s legitimacy. Validated records are grouped into blocks.

- Adding Blocks to the Blockchain: Once validated, the new block is added to the blockchain. Each block contains a unique hash code linking it to the previous block, ensuring tamper-proof integrity.

Business Benefits of Blockchain Technology

Blockchain offers numerous advantages for businesses, including:

- Enhanced Security: Transactions on a blockchain are immutable and encrypted, reducing the risk of fraud and unauthorized access.

- Improved Transparency: With a public ledger, every transaction is traceable, fostering trust among stakeholders.

- Cost Efficiency: By eliminating intermediaries, blockchain reduces transaction fees and streamlines processes.

- Operational Efficiency: Real-time data updates lead to better decision-making and faster operations.

- Enhanced Traceability: Blockchain enables businesses to track the origin and status of goods in their supply chains.

- Blockchain as a Service (BaaS): Platforms like Microsoft Azure and IBM allow businesses to implement blockchain solutions without extensive technical expertise.

- Regulatory Compliance: Automated records help businesses adhere to regulations, minimizing the risk of penalties.

- Innovative Business Models: Blockchain supports new models like tokenization and decentralized finance (DeFi), enabling fractional ownership and novel investment opportunities.

Use Cases of Blockchain Technology

Blockchain is increasingly utilized across various sectors:

- Cryptocurrency: Beyond Bitcoin, numerous cryptocurrencies like Ethereum, Ripple, and Litecoin leverage blockchain for secure transactions.

- Smart Contracts: These self-executing contracts automate processes without the need for intermediaries, streamlining agreements.

- Banking and Finance: Financial institutions are adopting blockchain for faster transactions and reduced costs.

- Supply Chain Management: Industries like food production and manufacturing use blockchain to enhance transparency and traceability.

Conclusion

This Beginner’s Guide to Understanding Blockchain Technology highlights the potential of blockchain to revolutionize industries through its decentralized and transparent nature. While there are challenges, such as the complexity of development, the demand for skilled professionals continues to rise. If you’re interested in exploring blockchain solutions for your business, consider consulting with a specialized development company.

FAQs

- What is blockchain technology? Blockchain technology is a decentralized and distributed ledger that securely records transactions and data across a network of computers without needing a central authority.

- What is the purpose of blockchain technology? The primary purpose is to provide a secure and transparent way to record and verify transactions, applicable in finance, supply chain management, voting systems, and more.

- How does blockchain technology work? Blockchain works by using a network of computers (nodes) to verify and record transactions, linking them in blocks through unique hash codes.

- Is blockchain technology secure? Yes, its decentralized nature and advanced cryptographic techniques make it highly secure against data manipulation.

- Can I invest in blockchain technology? Yes, you can invest by purchasing cryptocurrencies, supporting blockchain startups, or using blockchain-based investment platforms. Always conduct thorough research before investing.

{kind=link}